Italian Investment Accounts

How to invest efficiently in Italy. Forza!

Dennis Riosa covers investing, the Italian way….

Italian Pension Funds

PIP – The Italian Individual Pension Plan

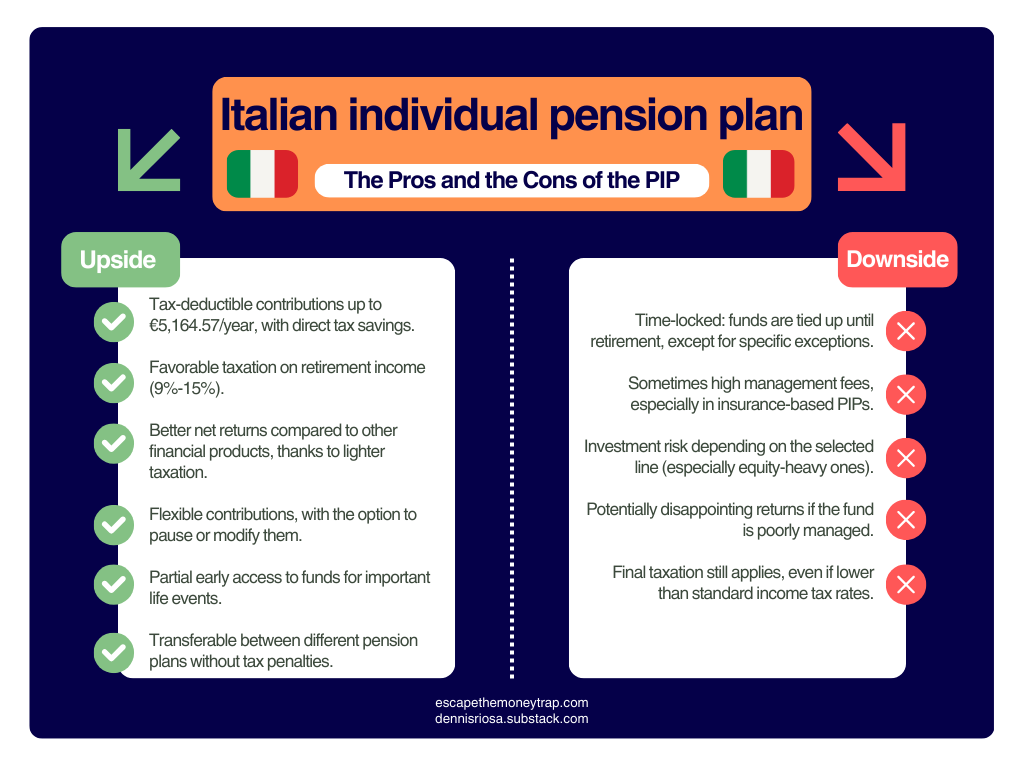

In Italy, there’s a very useful tool for those who want to supplement their public pension and build a more financially secure future: the PIP, or Piano Individuale Pensionistico (Individual Pension Plan).

This is a form of supplementary pension, regulated and incentivized by the state, that allows individuals to accumulate funds over time in view of retirement, with tax benefits and a fair degree of flexibility.

What is a PIP?

The Individual Pension Plan is a type of personal retirement savings scheme. It’s usually offered by insurance companies and is open to everyone: employees, self-employed workers, freelancers and even those currently not working. Participants make voluntary contributions into a pension fund, which is then used to pay out a supplementary income once retirement age is reached.

Subscribers can choose among different investment lines (ranging from low-risk to higher-risk strategies) depending on their risk tolerance and investment horizon.

How does it work?

The PIP operates in a straightforward way. Participants make periodic or one-off contributions, according to the contract, which can change over time. These contributions are then invested in specific fund lines (e.g., guaranteed, balanced,or equity-focused), managed by insurance companies or asset management firms.

Once the person reaches retirement age, the accumulated capital can be converted into a lifelong annuity or partially withdrawn as a lump sum (up to 50%) with the remainder paid out as an annuity.

Tax Benefits of the PIP

One of the main reasons why PIPs are attractive is the favorable tax treatment. Contributions are deductible from taxable income up to a maximum of €5,164.57 per year. This means that someone contributing, say, €5,000 in a year can reduce their taxable income and thus benefit from significant tax savings (up to over €2,000 for those in the highest tax bracket of 43%).

Moreover, the final payout is also subject to favorable taxation. The annuity is taxed at a substitute rate between 9% and 15%, much lower than the ordinary personal income tax rates. The investment returns within the fund are also taxed at a reduced rate of 20%, compared to the 26% applied to most other financial instruments.

Flexibility and Portability

PIPs are flexible tools. You can choose how much to contribute, pause your contributions at any time without penalties or modify the amount. If your job or career path changes, the accumulated capital can be transferred to another pension fund or PIP without losing the associated tax benefits.

Early Withdrawals and Redemptions

Before reaching retirement age, early withdrawals are allowed in specific cases: up to 75% of the capital can be accessed for serious medical expenses or for purchasing/renovating your primary residence. Aftereight years of participation, you can also request an advance of up to 30% for any reason. In certain situations (such as permanent disability or long-term unemployment), it’s possible to fully redeem the plan early.

Compared to tools like savings accounts, mutual funds or ETFs, PIPs offer a net tax advantage but with less liquidity and more restrictions. They are not suitable for short-term goals, but are ideal as long-term vehicles to complement the public pension system.

Unlike a standard brokerage account, PIPs don’t allow full freedom in selecting investments: you can only choose from the available management lines. However, for those with a long investment horizon and a high income tax rate, the tax benefits can easily outweigh the limitations in flexibility.

Conclusion

The Individual Pension Plan is one of the best options in Italy for building a complementary pension, especially for younger people or those with medium to high incomes. When used wisely, it can provide significant tax savings today and greater peace of mind tomorrow.

It’s often overlooked but it can be a cornerstone of a long-term financial independence strategy.

For anyone serious about managing their finances properly, the PIP isn’t just an option it’s a powerful, legal and underutilized fiscal lever.

Disclaimer: This content is for informational and educational purposes only. It does not constitute personal financial advice. Everyone’s situation is different — if in doubt, speak to a qualified, regulated financial adviser.

| A guest post by

|